In May 1938, or the ninth year of the Great Depression, a minister in Columbia County, Pennsylvania cast about for a sermon topic. In the past the minister, C.R. Ness, had spoken to the members of North Berwick Evangelical Church on a variety of themes: Paul’s Letter to the Philippians, the healing power of Jesus. He counseled families on their private lives, selecting topics such as “The Devotional Life of Men,” or “Traps for Young People.” This time, however, Reverend Ness chose the Book of Job.

And small wonder. By 1938, Columbia County felt like Job. The Book opens with Job at his prime, so righteous and prosperous he is known as “The Greatest Man of the East.” But God allows the Devil to play with Job and test him with trial upon trial. One after another, Job’s fortune, his family, his health are taken away. Since the beginning of the decade, Columbia County had endured its own series of trials –joblessness, shortages of cash, mortgage foreclosures, meals of only stewed tomatoes, or no meals at all. The siege was gradually wearing away citizens’ confidence in their own future.

“Why Do the Godly Suffer?,” Ness asked his flock. Was God testing Columbia County’s faith? “This will be a very timely series,” commented the editors of the local paper, the Berwick Enterprise. Job’s ancient travail, and his sustained faith, would console people now, “in these days of depression.”

Nor were Ness’s parishioners alone in their sense of desperation. In nearby Allentown, cash-short and underemployed citizens had, two years before, marched to the state capital and occupied the Senate gallery. Philadelphia, also nearby, had once been known as The Workshop of the World. No longer. In the early years of the Depression, hungry families revolted. Now two in ten still sought work.

Such troubles beset every region, and with such severity that Americans everywhere felt a sense of biblical retribution. Drought had plagued Western states for many seasons now, beggaring farmers. Black walls of dust, some a mile high, descended on farm towns, destroying crops and farms, and recalling the punishments in Job: “a great wind came from the wilderness, and smote the four corners of the house.” It was the Book of Exodus that crossed the mind of a columnist when another plague, grasshoppers, covered fields, devouring harvests. “Grasshoppers are locusts,” as in the plagues suffered by Pharaoh, wrote the columnist. The grasshoppers’ arrival was “the American equivalent of the Biblical plague that smote Egypt.”1 Later, the folksinger Woody Guthrie would recall that many believed they were suffering as the Egyptians had. “We watched the dust storm coming up like the Red Sea.”2

In the spring of 1938, when Ness sermonized on Job, unemployment in the building trades averaged more than 40%. Nationwide, one in five workers found themselves still jobless— or jobless yet again. It seemed that God was indeed smiting the land. Afterward, in the 1940s or 1950s, recalling their benumbed state, many Americans still treated the decade-long downturn as a divine test, or, more often, a great mystery, better left unexplored.

The eight mostly prosperous decades that have intervened since have only deepened the aura of mystery around the Depression. That is partly because the facts about the Depression lie outside the range of our experience. Today even the thought of unemployment greater than 10 percent spooks us; joblessness stayed stubbornly above the 10 percent line throughout the 1930s. Today we consider a rising stock market our national birthright. After the initial crash from a market high of 381 in 1929, the market stayed low for more than a generation, attaining its 1929 level only in the 1950s.

Further befogging the record have been those most equipped to illuminate it: scholars. Largely out of fealty to the President who led us during the Depression period, Franklin Roosevelt, many historians have been unwilling to probe the effect of Roosevelt’s multi-year recovery program, the New Deal. Economists, especially economics professors, will readily blame the rough post-crash period on the Federal Reserve’s failure to supply sufficient liquidity – money.

But with a few exceptions, the economics trade neglects the obvious next question. What about the years that followed? Why did recovery not return after five years, or after seven? It is not, after all, a deflation shock, however sharp, that converted the initial depression, lower case, into a Great Depression, with capital letters. It was the duration that made the Depression great. Whether monetarist or Keynesian, economists respond to commonsense queries about the later years with a single line: “That is complicated.” It is as if a sign has been placed over the period to intimidate the curious: “Here Be Dragons.”

Still, the duration of the Depression matters. These days, politicians routinely invoke the New Deal as a model of inspiration, without delving into the evidence of its effect. They do so even though the New Deal never, not even eight years in, met Roosevelt’s primary goal to “put America back to work.”

In reality, recovery’s absence in the 1930s is not so mysterious. Natural disasters contributed to the plight of the farms. The drought of the 1930s was unusually severe. The summers were unusually hot. While the “mighty wind” of the Dust Bowl resulted from a man-made eco-disaster: the overplowing of tens of thousands of acres.

The absence of a general recovery also can be explained. Recoveries, after all, are like people. They make choices. In each year of the 1930s, the recovery surveyed the economic landscape — and opted to stay away a while longer. Simple facts go a good way towards explaining why each year—and for slightly different reasons — the recovery absented itself. The same facts reveal the dangers of faith — not religious faith, but the political kind.

This story starts with the market crashes before 1929. These occurred with regularity as the Nineteenth Century closed and into the Twentieth. In those years, our laws did not task the federal government with managing the economy. When the economy stumbled, the economy had to right itself. The private sector, the belief was, would and should take the lead. Congress limited the federal government’s assignment to budget discipline that would keep the currency stable. Later, Congress created a new institution to aid the management of money, the Federal Reserve. Most relief work, however, was the work of the states.

In such a situation, the market determines how far prices fall. Even the price of labor. Nor is this necessarily evil. When businesses are less profitable, employers have fewer funds for wages. The obvious move for employers is to reduce wages. Most workers prefer lower pay to losing their jobs altogether.

In the early 1920s, as James Grant has shown, Washington and the young Fed addressed a severe downturn by halving federal spending and raising interest rates. These moves would today be considered counterintuitive, to put it politely. In the same period, a new president, Warren Harding, sent a signal: there was no need for grand reform from the government, despite the downturn. Grand reforms might impede recovery; what business needed was the assurance that giant changes from the government would not be forthcoming. “No altered system will work a miracle,” said Harding. “Any wild experiment will only add to the confusion. Our best assurance lies in efficient administration of our proven system.” Assailing the heavy burden of taxes postwar, Harding, once elected, made it clear to the public that he intended to reduce taxes wherever and whenever he could. Fewer burdens would free the private sector to pull the country forward.

It did. Indeed, the economy recovered so rapidly that the early 1920s downturn is today known as The Forgotten Depression. Stock prices rose dramatically, more than tripling over the decade. Jobs materialized, and most importantly, the standard of living increased. Productivity gains meant the old six-day work week could drop to five days. That gave America a gift we still enjoy: Saturday. Perhaps the best symbol of the general 1920s acceleration came from Henry Ford’s production line. At the beginning of the decade the standard car, the Model T, could reach the impressive speed of 40 miles per hour. But the Model A, sold from 1927, moved at 55 or 60 miles per hour.

When the Dow Jones Industrial Average accelerated, moving up by more than half within the course of a year, citizens of course expected some kind of market crash. The fall of 1929 brought that crash. Beyond inflated share prices, other factors, well documented by the extensive studies of the early years, exacerbated the subsequent downturn: the young Fed’s missteps, an international crisis, the collapse of vulnerable small banks across the land. Congress passed, and President Herbert Hoover went along with, a damaging tariff, Smoot-Hawley. Hoover’s tolerance of tariffs is particularly regrettable since Hoover knew better: his insights on the costs of the perverse policies at Versailles were so trenchant they won praise from even that most judgmental of colleagues, John Maynard Keynes. The 1929 plunge of the Dow was dramatic, but from November, the market began to move up smartly, from a low of 199 to 294 in April of 1930. The three preceding downturns had averaged 15 months in duration.3 Therefore citizens reasoned, just as they might today: “All things being equal, the recovery will come soon.”

But this time, all things were not equal. For Hoover, unlike Harding or his successor Calvin Coolidge, was inclined to action. Indeed, Hoover’s very reputation as a rescuer was what had brought this nonpolitician, engineer, and investor to the Presidency. Hoover had made his name in World War I, by organizing and seeing through a program to feed starving Belgians behind enemy lines. Further fame had come to Hoover when he directed a program to feed revolutionary Russia. Now Hoover ached to mount the most glorious rescue of all, the rescue of the American economy.

Hoover therefore turned to measures his “do less” predecessors would have eschewed. Rather than allowing the financial markets to bottom out, Hoover tried to stop their drop, personally, by railing against short sellers, whom he characterized pejoratively as those who conduct “raids on our markets with purpose to profit.” Hoover loaded burdens on business with a large tax hike, raising the top income tax rate to 63% from 25%. Even Hoover’s smaller interventions today look perverse: At a time when transactions were difficult, Hoover threw sand in the gears by introducing a tax on checks. As the President’s machinations proceeded, the banking crisis deepened, and the Dow plunged again.

Not content with meddling in markets, Hoover likewise tried to manage prices in another new area: labor. The economy wasn’t producing enough. Under a then-novel theory, higher wages would prompt recovery because they would invigorate workers and enable workers to spend more, stimulating the economy. Production, Hoover said, “depends upon a widening range of consumption only to be obtained from other purchasing power of high real wages.” As Lee Ohanian of UCLA has noted, through a combination of suasion and brute pressure, Hoover drove employers to raise the average real manufacturing wage by 10 percent.4

In 1931, Hoover and Congress codified their wage drive with passage of the Davis-Bacon Act. The official purpose of Davis-Bacon was to boost the economy through federal spending on construction projects in the states. But the law also mandated that builders pay “prevailing wages,” which translated to higher wages, for Washington and unions had a hand in setting levels. Strapped firms had to comply if they wanted the contracts –-but could hardly afford the wages. So the firms cut worker hours — dramatically—hired fewer workers or rehired more slowly. Bank failures did their damage. So did scarce credit. Still, the pressure on wages matters more than the history books convey. By 1932 joblessness hit 25 percent. The same year, the Dow Jones Industrial Average plunged further, dropping to 41.2 in July 1932, or almost 90 percent off its 1929 high.

Such stunning numbers—yet more stunning because they came years into the downturn—struck many Americans dumb. Others thought to reverse troubles through protest. In 1932, some 25,000 veterans converged on Washington to demand the government advance their “bonus,” a pension package set to be paid in 1945. Congress deadlocked, and for months the vets camped off Capitol Hill. Eventually, the President sent federal troops to clear the camps, torching their makeshift shelters. One of the presidential candidates that year, Franklin Roosevelt of New York, occasionally made conservative speeches, vowing to cut federal spending. Roosevelt likewise promised to help the worker, whom he characterized as “the forgotten man at the bottom of the economic pyramid.” But in other speeches, Roosevelt, like a politician from our own day, tried out class war rhetoric, assailing “princes of property.”

Though Roosevelt hardly made clear which policies he would promulgate, voters in 1932 opted for change and elected him. Over the winter of 1932-1933 rounds of bank failures amped up national anxiety. Like Hoover before him, the new president rejected Harding’s “no change” rule. Indeed, Roosevelt promised the opposite: “bold, persistent experimentation,” action for action’s sake, so much action that Roosevelt made Hoover look tame.

By the spring of 1933, the normally can-do American public was ready to go along with new interventions. Americans went along with, even savored, Roosevelt’s growing habit of scapegoating business. They also accepted the notion that Roosevelt’s experts, a clutch of professors quickly nicknamed the Brains Trust, knew better than they. Roosevelt was presented as a kind of political pastor, and Americans warmed to that, too. Today presidents who speak through new media gain special popularity: think of Donald Trump on X. Then, a new medium also worked magic: the radio. As Americans sat in their living rooms, Roosevelt’s disembodied voice reassured them: “The only thing we have to fear is fear, itself.” Soon Roosevelt was delivering routine talks to the American population, his Fireside Chats. “Even if what he does is wrong, they are with him,” commented the humorist Will Rogers of the electorate and Roosevelt at inauguration time. “If he burned down the Capitol we would cheer and say, “Well we at least got a fire started, anyhow.”

The dire situation offered Roosevelt a license available to none of his predecessors, at least not in peacetime: the license to direct the entire economy, from monetary policy to Wall Street, industry, agriculture, and even then-new industries, such as utilities. With his New Deal, the President claimed that license. In the famous 100 Days, his first legislative drive, Roosevelt established dozens of large programs to oversee or alter virtually every sector of the economy.

The National Recovery Administration, tasked with managing the industry, became the centerpiece of the New Deal. It was no accident the President selected a brigadier general, Hugh Johnson, to lead the National Recovery Administration (NRA), and a blue eagle as the NRA’s symbol. The NRA was to be a kind of military campaign, demanding suspension of disbelief. “Do not trifle with that bird,” warned Johnson.

Under statutes bearing visible traces of Benito Mussolini’s syndicalism, the NRA assigned large firms and industry leaders, to draft codes to promote efficiency in their markets. These codes spelled out in magnificent detail right down to what price a cleaner might charge to press pants, or which chicken a butcher must kill first — every aspect of daily business. One theory the NRA applied was a cartoon version of Henry Ford’s assembly line. Consumer choice at the counter slowed down commerce, the theory ran, and, the code’s authors maintained, slowed recovery. Fewer choices would accelerate the rate of transactions. Today, businesses make their money precisely because they offer consumers options. Starbucks comes to mind. Under the New Deal, such choice was suppressed.

Another principle embedded in the NRA was that wages and prices must stay high or move higher. All codes, as Lee Ohanian reports, set a minimum wage for lower-skilled workers, and most set wages for

higher-skilled workers as well.5 Thus did the New Deal scale Hoover’s higher-wage policy. That smaller businesses might be disadvantaged by codes crafted by industry giants, few dared discuss.

One who did was a tiremaker from Newark, Ohio, Carl Pharis. Pharis detailed his situation in a letter to Senator William Borah. Pharis Tire and Rubber was a small firm, which, through great discipline, held market share by producing “the best possible rubber tire” and selling at “the lowest price consistent with a modest but safe profit.” The NRA code imposed a price floor on tires that forced the prices of Pharis tires to the same levels as the tire giants. Under this system, even a firm loyal to the New Deal like Pharis’s would fail. “We are surely on our way to ruin,” Pharis told Borah.

The absurdity of these methods went overlooked, however, in part because they were put forth by great minds. This, even though the Brains Trusters displayed little awareness of how a business such as Pharis Tire and Rubber operated on the ground, or what roles consumers and sellers, individuals, might play in the marketplace. The most perspicacious of Roosevelt’s advisors, Raymond Moley, captured the myopic credentialism of his fellow Brain Truster, Felix Frankfurter:

The problems of economic life were [to Frankfurter] matters to be settled in a law office, a court room, or around a labor-management bargaining table “The government was the protagonist. Its agents were its lawyers and commissioners. The antagonists were big corporate lawyers. In the background were misty principals whom Frankfurter never really knew at first hand…These background figures were owners of the corporations, managers, workers and consumers.”

Those who dared to violate NRA rules confronted criminal charges and jail time: the NRA’s fathers had given their statute teeth. One company the Justice Department indicted was a small wholesale kosher butcher firm in Brooklyn, New York, Schechter Brothers. A third of their industry had already failed. To survive Schechter Poultry kept wages lower than the poultry code mandated. Paying wages that were too low was one of the many charges against them brought by the Justice Department. In the Schechters’ culture customers liked to pick their own chicken, as they had in the old live poultry markets of Europe. Choice was the Schechters’ market advantage over their new antagonist, the supermarkets. The poultry code held that the butchers must hand the buyer the first chicken that came into their hands. The Schechters’ feared, legitimately enough, that denying their buyers this option would lose them business—and allowed customers to continue choosing. That emerged as another count against them.

To win in public or in court, the Roosevelt Administration routinely resorted to intellectual bullying. In the Schechter case a federal prosecutor, Walter Lyman Rice, listened as one chicken dealer, named Louis Spatz, explained that he liked to set prices low to win customers, “same as any other business.” This common-sense the prosecution treated as primitive ignorance. An exchange between Rice, a graduate of Harvard Law, on the one hand, and Spatz, an immigrant with little English, on the other, captures the confidence with which the New Deal pulled rank.

Rice: You are not an expert.

Spatz: I am experienced, but not an expert…

Rice: You have not studied agricultural economics….

Rice: Or any sort of economics?

Prosecution: What is your education?

Spatz: None, very little.

The Supreme Court put the bully in its place. In its 1935 opinion on Schechter, the justices unanimously struck down the entire NRA. The High Court was even confident enough to pun about their decision: the NRA must go, “bone and sinew,” as one justice put it. But in the meantime, the Administration tugged and shoved at the demand curve for other industries. Hunger was still common across the land. Yet the NRA’s corollary agency in agriculture, the Agricultural Adjustment Administration both forced and paid farmers to destroy their crops, again on the principle that less product would drive up prices. No potato farmer could produce more than five bushels of potatoes without a special permit. “Despite the millions of times those cabalistic letters have appeared in print,” wrote a columnist in 1935 of the AA, “not all understand fully what they mean.” In Maine, it is said, that some authorities even required that farmers pour poisonous blue dye on the extra potatoes, to ensure they were unsalable and inedible. In Texas, mules long trained to step over delicate cotton rows were now driven over those plants to destroy them. The mules balked, as the papers reported.6

Farmers hardly saw the logic in the crop reduction scheme, but cash short as they were, they found themselves reluctant to turn down the generous payments. In Texas, where Lyndon Johnson worked for the New Deal, farmers in 1934 received some $50 million for complying with the production cutback.

Consumers were franker. After six million piglets were slaughtered in the name of nudging up prices, a disconcerted housewife wrote to the Agriculture Secretary, Henry Wallace: “It just makes me sick all over to think how the government has killed millions of millions of little pigs.” As it happened the price increase that had followed was too violent, raising “pork prices until today we poor people cannot even look at a piece of bacon.”

The extent to which Roosevelt relished disruptive experiments becomes clear in accounts of Roosevelt’s efforts to deflate the currency. After committing to the gold standard, Roosevelt abruptly reversed course and, surprising even his advisors, announced in April 1933 that the U.S. was leaving the standard. The move, an effective surprise devaluation, rocked other nations, many likewise enduring downturns. American central bankers dispatched to a London Conference a few weeks later now considered their main work restoring comity among rattled foreign governments. But Roosevelt undermined his negotiators by lobbing another bomb, calling plans for stabilization a “specious fallacy.” Returning home, George Harrison of the New York Fed told others “He felt as if he had been kicked in the face by a mule.”7

When cutting the dollar from gold did not keep commodity prices at the levels he sought, Roosevelt undertook to do so himself. His method was direct purchases of gold on the open market. Even for an institution as large as the United States government, this was a puzzling move equivalent of trying to raise the level of the ocean by dropping in water with a thimble. One by one, Roosevelt drove from the Administration those alert to his fallacies. “We are entering on waters for which I have no charts,” a financial advisor to Roosevelt, James Warburg, said in his resignation letter. As Liaquat Ahamed reports in Lords of Finance, Britain’s central banker, Montagu Norman, reacted by saying “This is the most terrible thing that has happened.” Even the truest of Roosevelt loyalists, Henry Morgenthau, found himself confused by the fashion —from his bed, in the morning, after breakfast —in which Roosevelt set his gold purchase prices.

One morning, as Morgenthau recorded in his diary, FDR ordered the gold price up 21 cents. Why 21, Morgenthau asked. Because 21 was 3 x 7, Roosevelt replied, and three was a lucky number. “If anybody really knew how we set the gold price,” Morgenthau recorded, “they really would be frightened.”

Markets were. The Dow Jones Industrial Average slipped down again. This is not to say that the private sector gave up in 1993 and 1934. In the spirit of a then- popular children’s book, The Little Engine That Could, companies responded to their obstacles by simply pushing harder. As Alexander Field has shown in his book A Great Leap Forward, engineers and scientists at private companies strained mightily and produced innovations that enabled companies to do more with less: diesel replacing the steam engine in railroading, for example.8 A road network planned by the states in the 1920s was in the process of construction, making it easier for firms to ship goods around the country. But these efforts came under duress, despite the obstacles of new regulations and random interventions.

In every downturn, certain industries continue to grow and have the capacity to serve as a locomotive of recovery: the energy sector after the financial crisis of 2008 is a good example. The industry that had that magic potential in the 1930s was electricity. In each year of the Depression—except 1933—American households used more electricity than before.9 Utilities such as Commonwealth and Southern were commencing the expensive work of wiring even hard-to-reach rural areas.

Now the federal government entered this market. Its start was the establishment of the Tennessee Valley Authority, or TVA, which aimed to serve the South through hydropower. Soon after came the Rural Electrification Administration, or REA, to fund the wiring of farms. At first, power companies told themselves and shareholders they could work with the government. REA officials met with companies, who assumed the funding would subsidize their work laying lines. The press interpreted these events with similar optimism: “As 95% of the electric industry in this country is in the hands of private operating companies,” wrote the New York Times, “the administration’s public funds will be dispensed in that proportion.”10 Instead, the REA bypassed the companies and funded local cooperatives, new and willing to follow REA’s direction. For a while, competition ensued; when the REA’s co-ops threw up their own lines on a rural road, a private company quickly laid its own, to mark its own plans. New Dealers smeared these efforts as “spite lines.”11 Over time, it became clear that the REA and TVA together were not helping companies like Commonwealth and Southern. Rather, they were squeezing them out of the market in a pincer action.

After the pincers came the hammer. The Administration saw through the passage of a law governing the capital-intensive utilities industry: the 1935 Public Utilities Holding Company Act, or PUHCA. The private companies labeled the law “a death sentence” because PUHCA so constrained their ability to raise capital that they genuinely could not compete.

Even those industries not scapegoated suffered under the New Deal tax policy. Though Hoover had raised taxes, Roosevelt boosted them yet again, specifically targeting those who were most likely to create jobs through investment: top earners. On a theory we would call Keynesian — though John Maynard Keynes was just beginning to elucidate it—the Administration wanted businesses to overcome their prudent tendency to save in hard times and distribute their profits instantly to stimulate the economy. In 1936, Roosevelt set out to force businesses to do so by seeing through the passage of an undistributed profits tax of 27%. The levy came on top of the (also increased) corporate income tax.

The New Dealers practiced an early iteration of what we call lawfare, selecting and prosecuting political opponents and stars of industry for tax evasion. The Administration picked the symbol of 1920s prosperity, the former Treasury Secretary Andrew Mellon, for one show trial. The initial decision to order an audit had been made by Treasury Secretary Morgenthau over the protest of the Bureau of Internal Revenue intelligence unit head Elmer Irey, whose review of Mellon’s returns had not alarmed him. His own experience also probably told him that one of the authors of the tax code, Mellon, was unlikely to claim anything other than legal deductions.

But President Roosevelt made it clear he would not honor the American law’s traditional distinction between tax avoidance – legal deductions, say – and tax evasion—illegal moves. Over time it emerged that politics, not logic, drove the officials: ‘You can’t be too tough in this trial to suit me,” Morgenthau told the prosecutor, the future Supreme Court justice Robert Jackson. “I consider that Mr. Mellon is not on trial but Democracy and the privileged rich and I want to see who will win.”12 Mellon was largely exonerated, but only after years: he spent his eightieth birthday in a Manhattan courtroom. By the end, even liberal columnists such as Walter Lippmann reckoned the Mellon prosecution was a

“profound injustice.”

Some businesses dared to pipe up, suggesting that higher tax rates created a moral hazard of their own. “When you outrage a citizen’s sense of equity,” warned a spokesman for the Ford Motor Company, “you school him in evasion.” A Harvard friend of the President’s, Alexander Forbes, wrote later to the President to argue that those causes for which rich men took tax deductions, charities such as university research, often did better than the federal jobs programs the Administration now funded. These latter were mere temporary jobs, “boondoggle.” Roosevelt replied by impugning Forbes’ morals; in a national emergency, the righteous move was to pay even those taxes not required by the tax code. Roosevelt, now well at home in his role as minister to the national flock, did not hesitate to chide or shame. To a lawyer who asked about the courts’ treatment of tax avoidance, FDR would write in 1937: “Ask yourself what Christ would say about the American Bar and Bench were he to return today.”13

The seasons passed and the New Deal created tens of thousands of jobs through programs such as the Works Progress Administration, or the Public Works Administration. Those who claimed one of these jobs, or worked on the Civilian Conservation Corps, clearing forest, say, were truly glad of the employment. Even tens of thousands of make-work jobs, and even the billions spent on these posts did not bring joblessness down to what Americans considered tenable levels. As the election year 1936 dawned, unemployment remained close to two in ten.

Yet that year, the nation gave President Roosevelt a second term in a resounding landslide. Only two states, Vermont and Maine, declined to support the man and the New Deal. Though the landslide still warrants more study, some explanations for the victory are evident. Four years in, Roosevelt had indeed become something like a national father. Alf Landon, the Republican candidate, chose to offer the electorate a version of New Deal Lite, which gained him no votes.

Now more thoroughly intimidated—the duration was beginning to feel permanent – voters supported Roosevelt as passengers support a captain in a storm: it is too late for another choice.

Yet a third reason, doubtless the strongest, was Roosevelt’s exquisite preparation for the 1936 presidential contest. Through 1935 and 1936, as authors such as Burton Folsom have shown, the New Dealers found a way to please, support, and fund nearly every large bloc that mattered to the election’s outcome. In dark times, and no longer on the land, seniors in cities and towns sought a pension. Social Security became the law of the land in 1935. Labor unions sought laws that would give them more muscle to pressure firms to accept unionization. The 1935 Wagner Act gave them muscle and then some, enough to force unionization on a resistant giant like Henry Ford. For farmers, likewise, there was a gift: the subsidies flowed.

In swing states, as Folsom shows, New Deal outlays increased dramatically. And for governors and mayors — always influential in presidential contents— millions came for construction projects, sparing the states and towns the difficult task of raising taxes. Many elections are bought, but the 1936 election qualifies as the boughtest. The states, the commentator Raymond Clapper wrote in the Washington Post, now realized that it was important “to keep on the good side of Santa Claus.” To voters still struggling, however, this Santa Claus seemed like a necessary miracle.

Still, such unprecedented and cynical electioneering cost the country troubles that we continued to endure well into prosperity, and even today. Through its outlays, the government was not only squeezing out business but also squeezing out what remained of Tocqueville’s local America. The statistics tell the story: the twelve months of 1936 were the first peacetime year in American history that federal spending outpaced state and local spending. The following year, federal spending fell back – but only for that year. The federal government has dominated states ever since.

There was another cost in the political culture, one we likewise feel. Sensing the inevitability of victory, Roosevelt’s opponents took to sliming the Administration. Members of an opposing group, the Liberty League, pointed to the record, but also assailed Roosevelt personally, more unusual then than now. This venture into the mud did not profit those opponents. Roosevelt responded with not just mud but a kind of mudslide, assailing “business and financial monopoly.” In tones that would sound unstatesmanlike even in our own era of trash talk, he told Americans of his opponents that “I welcome their hatred.”

“I should like to have it said of my first administration,” the campaigning president said in the same speech, delivered just days before the election, “that in it these forces of selfishness and lust for power met their match. I should like to have it said of my second administration that in it these forces met their master.” Some voters relished the prospect of all-out class war; many more, one suspects, chose not to consider the consequences of such a declaration.

But businesses did consider them. After the election, when Roosevelt made good on his promises, launching a vigorous antitrust campaign, effectively the opposite policy of the early New Deal and the syndicate-friendly NRA. Now the New Deal officials, who had set prices, officially deplored the “disappearance of price competition.”14 New actions assailed the oil industry, tobacco manufacturers were convicted of colluding absent proof of meetings or agreements, a daunting precedent. Companies reeled. It was in this period that utilities surrendered; Wendell Willkie of Commonwealth and Southern even sold part of the company to the TVA. After waiting politely through the 1936 election, labor unions used their new power to mount an unprecedented series of strikes, even occupying factories in so-called “sit-down strikes.” As Roosevelt’s own Labor Department mournfully reported:

“There were 4,740 strikes which began in the United States during 1937, in which 1,860,621 workers were involved. These workers lost approximately 28,425,000 man-days of work while strikes were in progress during the year.”15

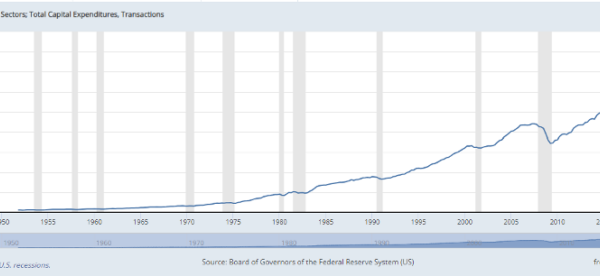

Each of these man-days lost postponed recovery. To halt the strikes, employers again paid higher wages than otherwise. Again, that constraint forced them to rehire more slowly. Companies despaired and went on strike themselves: net domestic private investment, the statistic that measures a company’s capacity to increase productivity, had been negative earlier in the Depression. In 1938 the measure turned negative yet again.16 A new Federal Reserve law increased the amount of cash banks had to hold in reserve; anxious, the banks held far more than officials had predicted, contracting credit. As Robert Wright shows in a forthcoming history of the period, even Social Security, which many Americans today rate the best of the New Deal, impeded recovery in the later 1930s: the few paycheck dollars held back by the government as worker payments were dollars that went unspent and uninvested.

Workers mulled the failure of relief programs. There was a new awareness of the degradation that came with competing with neighbors for federal benefits. Voters even reconsidered Roosevelt’s promise to help the Forgotten Man. Their mood resembled that of an editorialist in Muncie, Indiana who had published on the question two years before.17 “Who is the Forgotten Man in Muncie? I know him as intimately as I know my own undershirt. He is the man who is trying to get along without public relief and has been attempting the same thing since the Depression cracked down on him. He is too proud to accept relief yet deserves it more than three-quarters of those who are getting it.” This 1938 period came to be known as the “Depression within

the Depression.”

Preparing for the 1938 midterm election, the President sought during the primaries to drive out disloyal Democrats, even as he tried to give the appearance of impartiality. But this time, Moley later recalled, “the “mysticism did not sit well with the country.”18 While they might repeat the Job story at church, they were now beginning to realize that populist slogans are no substitute for prosperity, and voted accordingly, weakening the President’s majorities in both houses. Roosevelt himself began to weary of the New Deal.

The flood of new laws slowed which is certainly one reason the nation finally began to recover in 1939 and 1940. Many have argued that the dramatic rise in federal spending to support Britain in its war with Germany facilitated the comeback and that the further billions in outlays that came after Pearl Harbor guaranteed it. But another factor was perhaps more important: Roosevelt turned to the war long before Pearl Harbor. To arm Britain – and then America – he needed to ally himself with great companies and drop his domestic class war. Relieved businesses appreciated the ceasefire and began to produce and hire accordingly.

Historian Robert Higgs has developed a useful thesis to explain this lost decade: “regime uncertainty,” the notion that an erratic, aggressive government can terrify businesses into slowdown. The same theme was taken up by the chief economist of Chase Bank, Benjamin Anderson in a 1945 book, Economics and the Public Welfare. Though individual policies promulgated during the Depression may have differed, Anderson noted, there was one commonality: authorities’ arrogance. “Preceding chapters,” concluded Anderson at the end of his section on the Great Depression, “have explained the Great Depression of 1930–1939 as due to the efforts of governments, and very especially of the Government of the United States, to play God.” When playing God failed, Anderson noted, our government had determined that “far from retiring from the role of God,” it “must play God yet more vigorously.”19

What is the relevance for our own fractious age, and our own future downturns? The first point is that realization comes gradually: Americans did not see all the errors in the New Deal at first. Another point is that policy matters. When we belabor, lame, or derail the private sector, we reduce the likelihood of strong recovery. A third is that countercyclical spending, now institutionalized as the standard antidote to downturns, may not deliver all we imagine. Perhaps the federal response to the early 1920s is the better model. However severe the initial monetary challenges, the downturn after 1929 would not have become the Great Depression had Presidents Hoover and Roosevelt replayed the restrained federal policy of the early 1920s: reduce uncertainty and allow the market to take the lead.

The Depression also shows that we underrate the damage of bitter partisan attacks. There is a price to slinging the first mud in a conflict, and a price to descending into the dirt with your opponent. Had the opposition to Roosevelt been stronger, clearer, and less demagogic, it would have had wielded more influence. Another point, that of Robert Higgs, also warrants underscoring: the uncertainty generated by a power-happy demagogue, or an arrogant regime, costs all of us more than standard texts convey.

Yet a final thought, especially relevant now, involves the cost of politicizing economics. Any of us can understand that politicians must back silly or profoundly perverse policies to win an election. Many advocates of free markets will vote for candidates who emphasize anti-market concessions during campaign season, consoling themselves with the fact that the same campaigners, in a kind of aside, occasionally pay lip service to the power of markets. The voter, sometimes naively, hopes that once secure in office, the politicians will deliver the free-market policy. Sometimes, they do.

What is truly insidious however is when politicians advertise those subpar policies, from tariffs to, say, child credits or make-work jobs, as optimal economics, a guarantee of prosperity. For then, at least for a while, voters believe them. That is what happened in the 1930s. In such cases, the public, like the long-suffering 1930s electorate, becomes complicit in its own deception and disappointment.

In short, there is a price for placing faith in political leaders as one would in a church, a price for which voters are also responsible. “Have we found our happy valley?” Roosevelt asked when he called for a political license to continue his experimentation from on high in 1936. By reelecting him, even those many voters who did not have New Deal jobs agreed to continue to travel behind Roosevelt in his quest, and to tolerate policy that, at some level, they knew could not deliver. The consequence of this complicity was that second term of Depression.

The Americans who succumbed to political lures and failed to wind down, halt, block, or attenuate the New Deal were our great grandparents, or at the very least, our forerunners. Americans today owe it to them to forgive that error – and remember it. After all, they and we are one people. It is possible therefore to extend the sage Anderson’s point. The Great Depression did not endure because God struck America. It endured because our leaders played God. And because we let them.

References

Thorne, Frank, “Warning of Pest Heeded Too Late.” Buffalo News, July 11. 1936.

Ken Burns, 2012. “Bonus Material.” The Dust Bowl. Public Broadcasting Service.

Museum of American Finance. Banking Panics, 1930-1931. Richard Sylla. https://www.moaf.org/publications-collections/financial-history-magazine/82/_res/id=Attachments/index=0/Article_82.pdf (https://www.federalreservehistory.org/essays/banking-panics-1930-31)

Ohanian, Lee. E. “What, or who—started the Great Depression?” Working Paper 15258, National Bureau of Economic Research, 2009.

Cole, Harold L. and Lee Ohanian. New Deal Policies and the Persistence of the Great Depression: A General Equilibrium Analysis. Journal of Political Economy, Vol. 112, No. 4.

Pegler, Westbrook. “New Farming Theories.” Chicago Tribune Service, August 30, 1933.

Ahamed, Liaquat, Lords of Finance: The Bankers Who Broke the World, New York, Penguin Press, 2009.

Field, Alexander. A Great Leap Forward: the 1930s Depression and U.S. Economic Growth. New Haven: Yale University Press, 2012.

Historical Statistics of the United States, Colonial Times to 1957, Series S 81-93, “Use of Electric Energy: 2902 to 1956, p. 511.

Hirsh, Richard F., Powering American Farms: The Overlooked Origins of Rural Electrification. Baltimore: Johns Hopkins University Press, 2022.

Chayes, Antonia H., 1951. “Restrictions on Rural Electrification Cooperatives” Yale Law Journal. no. 61.

John Morton Blum, Ed. From the Morgenthau Diaries: Years of Crisis, 1928-1938, Boston: Houghton Mifflin, 1959.

Martin, George, CCB: The Life and Century of Charles C. Burlingham, New York: Hill and Wang, 2005 and Folsom, Burton W. Jr. 2008. New Deal or Raw Deal? How FDR’s Economic Legacy Has Damaged America, New York, Threshold Editions.

Roosevelt, Franklin. “Message to Congress on Curbing Monopolies,” 1938.

Monthly Labor Review, May 1938. United States Department of Labor.

Net Private Domestic Investment: Net Fixed Investment, Series A560RC1A027NBEA, Federal Reserve Bank of St. Louis, U.S. Bureau of Economic Analysis. https://fred.stlouisfed.org/series/A560RC1A027NBEA, August 22, 2024.

Lynd, Robert S and Helen Merrell Lynd, Middletown in Transition: A Study in Cultural Conflict, New York: Harcourt Brace and Company. 1937.

Moley, Raymond, After Seven Years, New York: Harper and Brothers, 1938.

Anderson, Benjamin M, Economics and the Public Welfare, New York: Van Nostrand Company, 1949.